I DON’T KNOW

Now with that out of the way, let me tell you what I do know.

I do know that compounding does work and INR 2000 put into an investment in 1995 today gave me a dividend of INR8500 this year and the value of my investment today is more than INR150000/-.

You will get a lot of sites both serious ones and satirical ones who talk about showing you a path to becoming a billionaire. But when you look at where you are starting from and what you need to invest to achieve that kind of number, the amount is so huge that you never get started.

This was a case with me also for a long time. I always got around to starting my investment journey, but never did till 2013. Each time I had to let my brain take a decision on making an investment, I always procrastinated, so I put in automatic systematic investment plans, which deducted money from my bank account.

The issue is never about whether you will become a billionaire, the question is always about whether you will take action to get there. If you will take action consistently and let the magic of compounding work then you will at least reach the skies, if not the stars.

My suggestion and advice to all the young folks is always start with just a small amount which is not more than 10% of your income, but let it get deducted out of your bank account directly before you can touch it. Once you do that and not think about it, you will be surprised at what you will see after 25 – 50 years. As an example the average return on the S&P 500 has been more than 10%. Suppose you have $500 invested for 50 years in an ETF which only works on the S&P500 the number you could potential be looking at is close to $58K. So if you can avoid about 100 coffees & a doughtnut at your local coffee shop, you could be at more than 50K in 50 years. If you were to avoid it for only one year( $5*365) and invest that for 50 years you would be at about $214K. Can you save $25 in a day. Most people can. You could potentially be a millionaire, and that too just investing for 1 year.

The key point here is that you are investing – not saving. For the difference between the 2 please see my earlier blog posts.

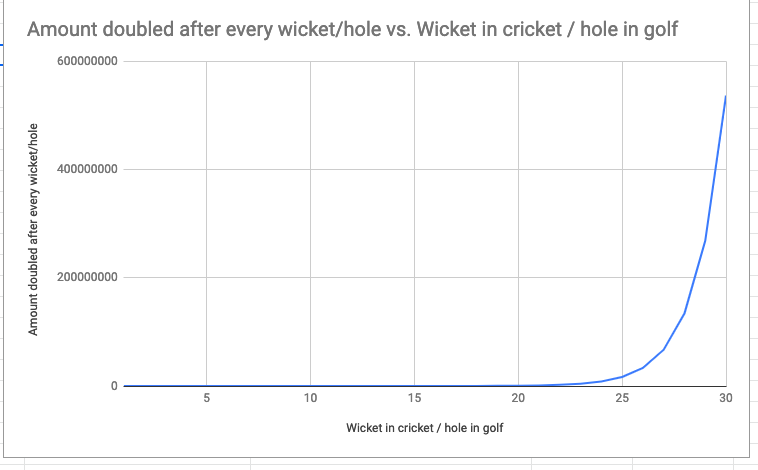

The earlier you start out on your investment journey, the higher will your corpus become. If you notice even Warren Buffet’s meteoric rise in becoming the richest man has been in the making for more than 60 years. Its the last 15 odd years where the compounding has created such an explosive growth in his wealth.

Start somewhere, start at the earliest, start with the smallest and let it compound.

Till next time.

Carpe Diem!!!