Last time I showed a graph and calculations of how a doubling of a bet for every cricket wicket or golf hole can make you a millionaire many times over if you allowed to take the bet over a large number of wickets.

The bigger part however is that the real advantage comes as you take the period over a longer term.

This time I will show you how the value of the bet can change the value of your earnings. As I have repeated many times in my blogs earlier also, the value of money you end up with is has low co-relation to the amount you start with but rather with the duration and the rate of interest.

So this time also we will start with only one dollar to start with and show you how the value of the amount you get depends at the rate at which you grow your bet. We will consider 8%, 15%, 17% and 24%. There is a reason for choosing these rates.

Typically a long term bank deposit in India can get you about 8%. Its almost guaranteed to not fail. So you don’t have to take any risk to get this kind of return.

15% -17% is the average return that the Indian stock market has returned on average. 24% is the kind of lowest return the investing gurus have been able to generate from the stock market.

| Wicket in cricket / hole in golf | Rate of interest 8% | Rate of interest 15% | Rate of interest 17% | Rate of interest 24% |

| 1 | 1.08 | 1.15 | 1.17 | 1.24 |

| 2 | 1.1664 | 1.3225 | 1.3689 | 1.5376 |

| 3 | 1.259712 | 1.520875 | 1.601613 | 1.906624 |

| 4 | 1.36048896 | 1.74900625 | 1.87388721 | 2.36421376 |

| 5 | 1.469328077 | 2.011357188 | 2.192448036 | 2.931625062 |

| 6 | 1.586874323 | 2.313060766 | 2.565164202 | 3.635215077 |

| 7 | 1.713824269 | 2.66001988 | 3.001242116 | 4.507666696 |

| 8 | 1.85093021 | 3.059022863 | 3.511453276 | 5.589506703 |

| 9 | 1.999004627 | 3.517876292 | 4.108400333 | 6.930988312 |

| 10 | 2.158924997 | 4.045557736 | 4.806828389 | 8.594425506 |

| 11 | 2.331638997 | 4.652391396 | 5.623989215 | 10.65708763 |

| 12 | 2.518170117 | 5.350250105 | 6.580067382 | 13.21478866 |

| 13 | 2.719623726 | 6.152787621 | 7.698678837 | 16.38633794 |

| 14 | 2.937193624 | 7.075705764 | 9.007454239 | 20.31905904 |

| 15 | 3.172169114 | 8.137061629 | 10.53872146 | 25.19563321 |

| 16 | 3.425942643 | 9.357620874 | 12.33030411 | 31.24258518 |

| 17 | 3.700018055 | 10.761264 | 14.42645581 | 38.74080563 |

| 18 | 3.996019499 | 12.37545361 | 16.87895329 | 48.03859898 |

| 19 | 4.315701059 | 14.23177165 | 19.74837535 | 59.56786273 |

| 20 | 4.660957144 | 16.36653739 | 23.10559916 | 73.86414979 |

| 21 | 5.033833715 | 18.821518 | 27.03355102 | 91.59154574 |

| 22 | 5.436540413 | 21.6447457 | 31.6292547 | 113.5735167 |

| 23 | 5.871463646 | 24.89145756 | 37.00622799 | 140.8311607 |

| 24 | 6.341180737 | 28.62517619 | 43.29728675 | 174.6306393 |

| 25 | 6.848475196 | 32.91895262 | 50.6578255 | 216.5419927 |

| 26 | 7.396353212 | 37.85679551 | 59.26965584 | 268.512071 |

| 27 | 7.988061469 | 43.53531484 | 69.34549733 | 332.954968 |

| 28 | 8.627106386 | 50.06561207 | 81.13423187 | 412.8641603 |

| 29 | 9.317274897 | 57.57545388 | 94.92705129 | 511.9515588 |

| 30 | 10.06265689 | 66.21177196 | 111.06465 | 634.8199329 |

If you see the difference between the 8% and 24% rate of interest is 3 times. However the outcome is 63 times different over 30 units. If you were to look at an even larger period like say 50 units the difference will come out to be 1000 times.

The human brain is not able to comprehend this major magic of compounding when trying to compute mentally.

Now look at the columns which are with showing you 15% and 17% interest rates. While the difference is only 2% if you see the outcome after 30 holes at 17% you have earned double then at 15%. If you were to extend this to 50 holes then the amount at 15% would be 1083 while at 17% it would be 2566. A difference of 2.5 times. Why am I showing you this. If you pay 2% commission to someone to manage your investment then you lose that kind of money.

The people like Warren Buffet or Raamdeo Aggarwal or Mohnish Pabrai have become so exorbitantly rich because they manage their own money and manage it a higher rate of interest for a longer period of time.

However even if you think you cannot manage on your own, its better to get some reputed ETF so that the cost of managing is very low. Only in cases of some high growth markets look for managers to manage specialised funds.

Another thing you will notice from the table – till about the 4th unit all the values were not very far apart. But see how the 24% chart suddenly breaks into another orbit after the 10th unit and the gap widens so dramatically.

The biggest lesson in this post and the earlier one is however that you need to start at the earliest, with whatever you have and let it compound over a long period of time.

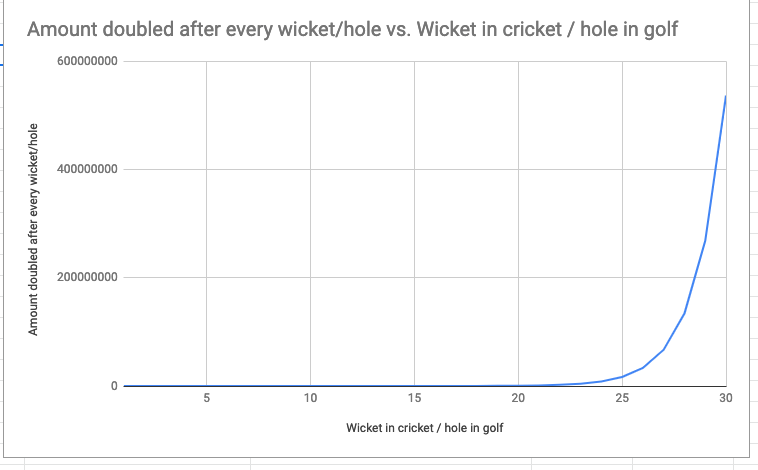

For those of you who are more visually inclined, you can have a look at the chart below

Till next time choose the right interest and keep it for a long long time

Carpe Diem!!!